Most first-time sellers have heard a horror story. Someone at the country club whose due diligence dragged on for a year. A friend of a friend whose deal fell apart three weeks before closing. A buyer who kept asking for more and more until the seller gave up.

Those stories are real. They are also the exception, and they usually trace back to a seller who walked in blind. Due diligence is demanding, but it runs in a fairly predictable order, and knowing that order ahead of time is most of the battle.

Due diligence is the period after a letter of intent is signed when a buyer verifies everything about your business before committing to the purchase. It is where a deal is confirmed, renegotiated, or lost. Understanding what is coming, in what order, why, and what not to do, is one of the most valuable things you can do before you ever sign an LOI.

Consider this a reality check on what actually happens.

How Long Due Diligence Takes

Due diligence begins once a letter of intent is signed. That makes the LOI itself critically important, because a number of terms need to be negotiated into it before this stage starts. Anything left undefined in the LOI may be resolved later in the buyer’s favor.

The duration varies widely. For very small businesses, it can be as short as 45 days. More commonly, buyers will talk through a 90 to 120 day window. A great deal of what determines where you land in that range comes down to how prepared you are before the process starts and how quickly you respond once it does.

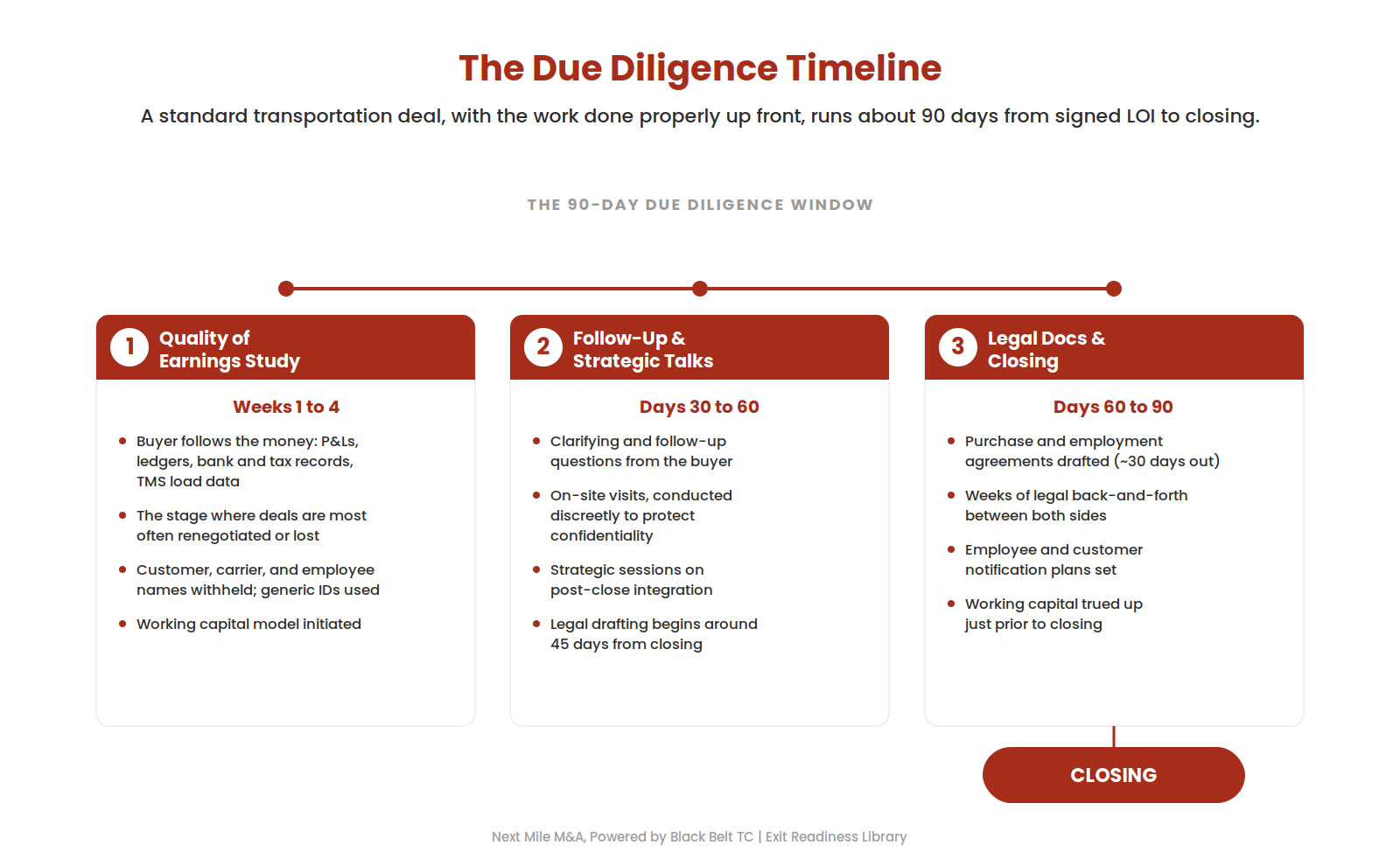

A standard due diligence period, with the work done properly up front, runs about 90 days from signed LOI to closing. The timeline below shows how that period typically breaks down. Each stage is covered in detail in the sections that follow.

Stage One: The Quality of Earnings Study

The first stage, and the one a seller should insist comes first, is the quality of earnings study, often called a Q of E. Not every buyer sequences it this way. Some jump straight into operational or legal review. But there is a strong reason to run the financial verification first: this is the stage where a buyer is most likely to change the terms of a deal or walk away from it entirely when necessary financial adjustments are found. It is better to clear that hurdle before anyone invests months in the rest of the process.

A Q of E is, at its core, a follow-the-money exercise. On larger deals, the buyer will often hire an outside accounting firm to perform it. They will request your P&Ls over extended periods, balance sheets, general ledgers, bank records, tax records, and load data from your TMS. The goal is to trace the entire financial life of a shipment, from the moment a load is booked through to when the receivable is collected, and confirm that everything reconciles.

A meaningful amount of legal review usually runs in parallel during this window, mostly high-level background checks and similar items.

What You Should Never Hand Over Too Early

There is one policy that experienced advisors stress and that unrepresented sellers routinely get wrong: names are not shared. Specifically, customer names, carrier names, and employee last names stay protected in the early stages. First names for employees are generally fine. Full employee data, last names and Social Security numbers, are not. Customer names are never provided in the load data either.

To make this work, you need a way to map every customer to a consistent generic identifier before the process starts. Customer XYZ becomes Customer One. Another becomes Customer Two. Those identifiers stay consistent throughout the Q of E so the buyer can analyze concentration, lanes, and pricing patterns without ever seeing who your customers actually are.

The reason is straightforward. The moment you hand a buyer your full load data with customer names attached, they have your lanes, your pricing, and your most valuable relationships, and if the deal falls through, they keep all of it. That risk climbs when you are dealing with a buyer you do not know, or working with an M&A firm that blasts a sales memorandum out into the open market. An NDA helps, but only so much. If a buyer uses what they learned in a way that is hard to trace, enforcing that NDA means litigation, proof, and years. We recently saw a seller who had engaged with a buyer without even an NDA in place. There is no taking that information back later.

Running the Data Room

Going into due diligence, you want a clearly defined single point of contact on each side. All communication flows through those two people. This matters more than it sounds, because most buyers bring multiple parties into the process: an outside accounting firm for the Q of E, an outside legal firm, and depending on the buyer’s size, internal safety, fleet, and HR people.

Every one of those parties can generate requests. Without discipline, the same question gets asked three different ways by three different people, and the seller is left digging through old emails trying to remember whether they already answered it. The fix is a working checklist inside the data room. As items are submitted, they are marked complete. Any new request, even one that comes up verbally or from the outside accounting firm, gets added to that checklist and posted as a live working file. The process is extensive and exhausting enough without redundant questions.

Stage Two: Follow-Up and Strategic Discussions

Once the Q of E is substantially complete, the process moves into follow-up questions, clarifications, and strategic conversations.

If on-site visits have not already happened, they typically occur here. This is a sensitive moment, because it intersects with one of the hardest questions a seller faces: when to tell employees. The recommendation at this stage is that any visit is conducted discreetly. A buyer wants to see the business in action, not an empty building after hours, but they also should not be walking the floor in a company-branded shirt announcing who they are. A visit can be framed as a customer, an insurance representative, or an accounting contact. The point is to let the buyer touch and feel the operation without disrupting it or tipping off the workforce before the seller is ready.

This is also when strategic discussions begin: how the buyer’s capabilities could be leveraged inside your organization, and how a post-acquisition integration might work. And it is when the legal documents start to take shape, usually around 45 days out from closing.

Stage Three: Legal Documents and Closing

The legal phase is where deal structure becomes deal paperwork. Depending on how the transaction is built, there can be several documents: a purchase agreement, which can be extensive, and potentially an equity agreement, an operational agreement, and employment agreements. The earnout itself is not negotiated here. It should have been already defined in the letter of intent, which is exactly why getting the LOI right matters so much. The more that was defined clearly up front, the less time and legal expense gets spent fighting over it now.

A seller should expect to see employment agreements and an initial draft of the purchase agreement around 30 days out from closing, with the understanding that several weeks of back-and-forth between the two legal teams is normal.

Why Your Choice of Legal Counsel Matters

This is the point where the proper legal firm becomes invaluable, and the wrong one becomes expensive. You want a firm with deep transportation acquisition experience, one that has dealt with the range of valuations and structures in the market and knows what genuinely counts as typical market terms. A firm like that knows where the reasonable middle ground sits on each point, because they have negotiated against buyer’s counsel many times before.

What you do not want is a firm that treats the agreement as a battlefield, marking up every line and bleeding red ink across the document to prove a point. As Wally Brauer puts it, that is not only an ego problem, it is an expense problem. Every additional point a legal team insists on fighting drives up cost and drags out the timeline. The best counsel can see a deal from both the buyer’s and the seller’s perspective and focus on what will actually get the transaction closed for everyone.

Working Capital

Most transportation deals, particularly those above $5 million in annual revenue, require that working capital stays in the business. Working capital is essentially the spread between your receivables and your payables.

By the end of the Q of E, there should already be an agreed understanding of how working capital will be calculated, with the buyer providing a working model and an initial calculation. A baseline figure is then set just before closing. That baseline is typically trued up about 90 days after closing, once the final numbers settle.

Post-Acquisition Integration

The strategic sessions carry into specific integration planning: how employees will be notified, how customers will be notified, and how the transition will be handled for different groups. These plans get tailored. Smaller customers might receive a general email. Larger customers often warrant face-to-face meetings so the transition is properly explained and no relationships are lost.

Most buyers want to avoid disrupting the business at all. They typically let a seller keep the brand name they built, often introducing soft transitional marketing over time, where invoices might eventually read “Seller XYZ, powered by Buyer QRS.” Integrations like moving onto the buyer’s TMS get discussed here too, since buyers generally want financial data flowing through their systems, though the timeframe for that can vary widely.

After Closing: The Working Capital True-Up

Closing is not quite the last step. Roughly 90 days after closing, the working capital baseline set just before the deal closed gets trued up against the final actual figures. It is mostly a cleanup item, but it is worth knowing it is coming.

How to Get Through It

Knowing the stages is the easy part. Actually getting through them, while still running your company, is where sellers struggle. A few things matter more than the rest.

Hit the checklist with everything you have. When the due diligence checklist arrives, the goal is to provide as much of it as possible, ideally all of it, within about two weeks. The faster you provide information, the faster the burden of the deal shifts off you and onto the buyer to process it. Slow responses do the opposite, and they extend the timeline exponentially. Many checklist items are linked, so if four of five connected items are submitted and the fifth shows up three weeks later, the buyer may not be able to start on any of them until the last piece arrives.

Understand that responsiveness is a signal. Due diligence is the buyer’s first real look at how you actually operate. Turn information around quickly and in good order and it builds confidence. Drag your feet or hand over a mess and the buyer starts wondering what they have gotten into. They are sizing up more than your numbers here.

Get help, because you already have a full-time job. A seller running a business does not suddenly have free time to manage a second full-time job. The sellers who navigate this best either have a strong right-hand person, often a COO, dedicated to assembling information, or a firm running alongside them to clarify what the buyer actually needs before they chase information down a rabbit hole. This is also where seller fatigue sets in for those who try to do it all themselves.

Keep running your business exactly as you always have. This one costs sellers real money when they get it wrong. Mike Bloss describes an early deal where two owners, having just agreed on a price, decided to give themselves each a $50,000 salary bump and two family members a $35,000 bump apiece. You cannot do that. Do not extract cash from the business. Do not suddenly change how you handle receivables and payables. Every one of those moves raises a flag and causes problems.

Because working capital is almost certainly going to be required, the smart move well ahead of the process is to focus on your cash flow: collect receivables diligently, get customers onto regular payment schedules, and pay your carriers on a timeline that keeps them hauling for you. What you cannot do is abruptly stretch your carrier payables from 14 days to 45 just to narrow the spread. A buyer will find it, and it will cause problems. The general rule is simple: manage the business the same way you always have.

The Next Mile Difference

Everything above is true regardless of who represents you. Where representation changes the outcome is in how much of this is handled before a buyer is ever in the picture.

Next Mile M&A built its process around running a high-level quality of earnings analysis up front, through proprietary technology and automation, before a seller goes to market. That process has caught EBITDA errors totaling more than $2 million in financial numbers that, left undiscovered, would have dramatically affected valuations or caused buyers to withdraw mid-process. Catching them first, instead of letting a buyer’s accounting firm surface them during the Q of E, is what keeps a deal from getting reopened later.

It is also, by Mike’s knowledge, the only firm that collects TMS load data up front, because it is the only firm with the proprietary technology to process it. Since a buyer is going to match load data against financial data anyway, doing that reconciliation before going to market takes out a major source of delay and renegotiation risk.

There is a human side to this too. Wally Brauer, who sold Freight Solutions in a life-changing transaction, went into due diligence with a strong COO handling the checklist and Mike Bloss alongside him. He describes the emotional reality of the process and what made the difference for him:

“Going into it, there is a lot of excitement and a lot of angst. This is really happening now. You want confidence that whatever M&A firm you are dealing with is going to be there through all the hurdles, the ups and the downs. That is very important.”

Wally had been the seller himself. That is a different thing from advising one, and in the hard moments of a deal it matters more than most people expect.

The Bottom Line

Due diligence is demanding work, and now you have a rough map of how it unfolds. It moves through a quality of earnings study, follow-up and strategic discussions, and a legal and closing phase, with a working capital true-up after the fact. The sellers who come through it with the deal they were offered are the ones who understood the path before they started, protected their information, responded quickly, kept running their business the same way, and had experienced people alongside them.

The horror stories almost always share the same root: a seller who went in without a plan, without protection, and without anyone in their corner who had done this before. You now know what is coming, which is exactly what those sellers did not.

Ready to Understand What Due Diligence Would Look Like for Your Business?

If you are thinking seriously about an exit, the most useful thing you can do is understand what a buyer is going to put your business through before you are in the middle of it. We will walk through your specific situation, show you where the risks are, and give you an honest read on how prepared you are.

No obligation. No pressure. Just a straight conversation from people who have been on both sides of these deals.

Schedule a Confidential Consultation

Next Mile M&A, Powered by Black Belt TC, was founded to handle the work outlined in this article before a seller ever goes to market. Mike Bloss built a proprietary process to surface financial and operational issues up front, so a seller can correct what is correctable and walk into due diligence prepared, rather than spending six to nine exhausting months discovering problems a buyer found first.